Car insurance bills keep climbing, and 2025 isn’t giving drivers much of a break. But finding the Best Car Insurance Quotes this year can make a big difference in your budget. You don’t have to settle for the first renewal number your insurer sends. With smart shopping and a few insider tips, you can cut your monthly bill while still keeping the protection you need. Let’s break down why rates are up and how you can save big in 2025.

1. Why Car Insurance Rates Are Higher in 2025

If your premium feels more expensive this year, you’re not imagining things. Repair costs are still way up thanks to pricey parts and labor. Extreme weather—hurricanes, wildfires, hail—means insurers are paying out more claims and passing that cost back to drivers. Supply chain hiccups and tariffs are making it harder (and more expensive) to fix cars. On top of that, rising medical bills, lawsuits, and thefts all drive premiums higher. Nationwide, rates are still going up, though not as fast as in the past few years.

2. Factors That Shape the Best Car Insurance Quotes

Insurance companies look at a bunch of things when they set your rate. Your driving record is the biggest one—tickets, accidents, and DUIs will hike your premium fast. Credit score matters too in most states: better score, better rate. Age and experience count, which is why younger drivers pay the most until they hit about 25. Where you live also plays a huge role: city ZIP codes mean more accidents and thefts, so higher premiums. The car you drive, how far you drive it, and the coverage you pick all shape your final quote.

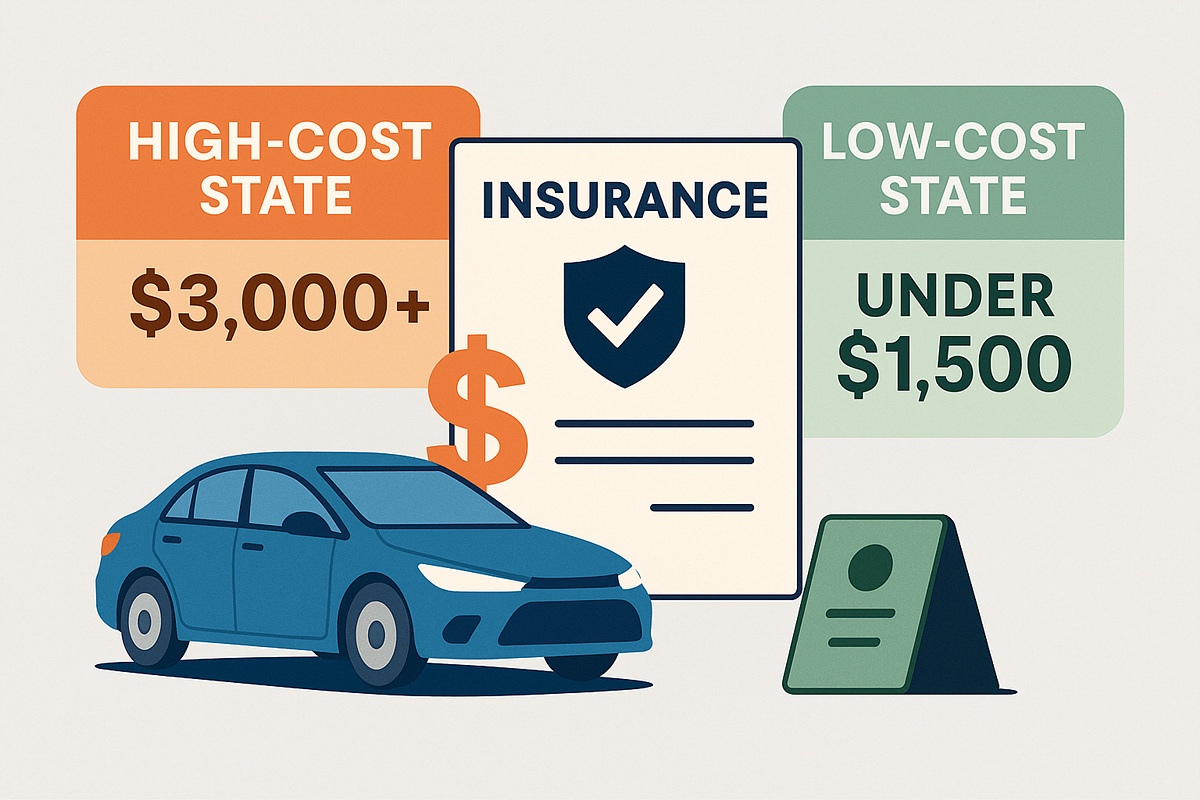

3. Average Costs and Cheap Car Insurance Rates in 2025

The national average for full coverage in 2025 is around $2,101 a year. In high-cost states like Florida, New York, or California, full coverage often tops $3,000 annually. Meanwhile, drivers in cheaper states like Idaho may see bills under $1,500. If you’ve got a clean record and an older car, switching to liability-only coverage can unlock Cheap Car Insurance Rates, sometimes cutting your bill by 50% or more.

4. Smart Ways to Save on Car Insurance USA

There are plenty of ways to reduce your premium, and they’re easier than you might think. Shop around—don’t just stay with your current company out of habit. A quick quote check every 6–12 months could save you hundreds. Raise your deductible if you can handle the risk; your monthly bill will drop right away. Driving an older car? Skip the expensive collision or comp coverage. Bundle your auto with home or renters insurance for an instant discount. Don’t miss out on easy extras like safe-driver rewards, good student discounts, low-mileage programs, and defensive driving courses. These small steps can help you Save on Car Insurance USA.

5. Quick Checklist Before You Renew

- ✅ Make sure your liability coverage meets state minimums (and consider going higher for peace of mind).

- ✅ Always grab at least three quotes with the same coverage for apples-to-apples comparison.

- ✅ Ask about every possible discount—some agents won’t volunteer them.

- ✅ Double-check your ZIP code and garaging address since rates can change even within the same city.

- ✅ If you don’t drive much, look into usage-based or pay-per-mile plans.

- ✅ Balance your deductible and premium; sometimes raising your deductible a bit can save hundreds a year.

6. When Paying More Makes Sense

Sometimes cheaper isn’t better. If your car is brand new, leased, or financed, your lender will require full coverage anyway. If you live in a storm-prone or high-theft area, cutting coverage could leave you exposed. Long commutes or heavy business use may justify stronger protection. And if you have assets to protect, higher liability limits are worth the extra cost.

7. Trends to Watch in 2025 and Beyond

Some states are starting to regulate rate hikes, which could stabilize costs. Usage-based insurance is expanding, rewarding drivers who drive fewer miles or show safer habits. Electric vehicles keep growing, but their repair costs still mean higher premiums. Global supply chain issues and tariffs also remain unpredictable, which could impact repair costs and future insurance pricing.

Conclusion

Car insurance premiums in 2025 may be high, but finding the Best Car Insurance Quotes and making smart adjustments can save you real money. Compare quotes, raise your deductible if it makes sense, use discounts, and tailor your coverage wisely. With the right moves, you’ll keep your wallet safe while staying protected on the road. staying protected on the road. Take action before your renewal, and you’ll thank yourself later.

Q: Should I always pick the cheapest quote?

Not necessarily. The cheapest option might mean bare-bones coverage, high deductibles, or bad customer service. Always check what’s actually covered and how claims are handled.

Q: Does safe driving really lower my rate?

Absolutely. A clean driving record is one of the fastest ways to bring your premium down. Many companies also give extra discounts for safe-driver programs and defensive driving courses.

Q: How much can bundling really save me?

It depends on the company, but many drivers save anywhere from 5% to 25% when they combine auto with homeowners or renters insurance.